How Accessing the Private Investor Market for Selling Commercial Real Estate Loans

KEY TAKEAWAYS

The Commercial Real Estate Foundation is Cracking.

In the aftermath of the liquidity crisis in 2023, during which several regional banks failed due to mismanagement of their liquidity positions, financial institutions have been under heightened regulatory scrutiny. The crisis underscored the importance of robust liquidity management, credit monitoring and operational efficiency.

The convergence of high lending rates, decreasing commercial real estate values, $2 trillion in near-term commercial loan maturities, declining deposit balances, increasing cost of funds, and the lurking risk of potential economic recession, has created a perfect storm of credit and liquidity risk.

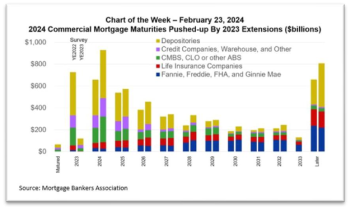

It has been chronicled that commercial real estate loan portfolios are under increasing pressure. The impending troubled commercial real estate market is facing a record volume of maturing loans, significantly increasing prospects for a surge in defaults as property owners are forced to refinance at higher rates.

According to national accounting firm Moss Adams, LLP, “The risk of default of near-term

maturities has risen in recent months creating a debt dilemma in the commercial real estate

industry that presents real estate investors with tough decisions. $650 billion in commercial loan

maturities are expected in 2024 and in 2025 an additional $570 billion in loans are scheduled to reach maturity, followed by $460 billion in 2026. In total, approximately $2 trillion of commercial

real estate mortgages are

scheduled to reach maturity

from 2024 through the end of

2026. The largest share is

multifamily, accounting for

approximately 33% of

maturing loan volume. While

many of these loans are

performing, maturing loans

will require refinancing, or,

possibly asset disposition, as

borrowers face the largest

disruption in borrowing

activity since the 2007-2009

recession. Compounding the issue, the rise in borrowing costs, primarily from higher interest rates

and more restrictive covenants, comes at a time when asset values are falling.

According to national accounting firm Moss Adams, LLP, “The risk of default of near-term

maturities has risen in recent months creating a debt dilemma in the commercial real estate

industry that presents real estate investors with tough decisions. $650 billion in commercial loan

maturities are expected in 2024 and in 2025 an additional $570 billion in loans are scheduled to reach maturity, followed by $460 billion in 2026. In total, approximately $2 trillion of commercial

real estate mortgages are

scheduled to reach maturity

from 2024 through the end of

2026. The largest share is

multifamily, accounting for

approximately 33% of

maturing loan volume. While

many of these loans are

performing, maturing loans

will require refinancing, or,

possibly asset disposition, as

borrowers face the largest

disruption in borrowing

activity since the 2007-2009

recession. Compounding the issue, the rise in borrowing costs, primarily from higher interest rates

and more restrictive covenants, comes at a time when asset values are falling.

To read complet whitepaper - Click Here